Curious about what keeps experts, CEOs and other decision-makers in the Intelligent Document Processing (IDP) space on their toes? Get food for thought on IDP-related topics from the industry’s leading minds.

In this opinion piece, Petra Beck, Senior Industry Analyst at analyst firm Infosource, examines the state of the IDP industry and how technological advances and corporate enterprise are changing both vendor strategies and buyer priorities.

The global Intelligent Document Processing (IDP) market is increasingly shaped by sector priorities, evolving use case complexity, and enterprise readiness for GenAI-driven transformation. Drawing on Infosource’s in-depth assessment of the global IDP market and building on my last opinion piece for this publication, I highlight where growth is strongest to date and how evolving technology and enterprise readiness are redefining both vendor strategies and buyer priorities. What defines this next chapter is not just technological progress, but the interest in autonomous end-to-end process automation. This assessment distills key market data and predictions that will shape IDP’s future trajectory.

IDP Market Trajectory: 2024 Momentum and Scenarios

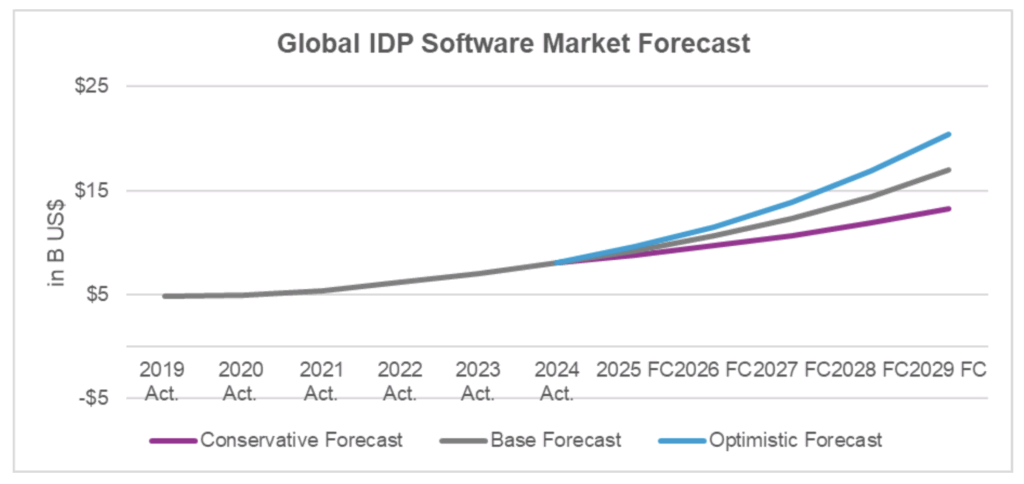

Global IDP demand surged to $8 billion in 2024, growing at 14.5% year-over-year as enterprises accelerated automation and adopted GenAI for unstructured data workloads. In the base case forecast Infosource projects a 16% CAGR through 2029, with further acceleration expected as agentic automation advances from pilot to production. Scenario analysis illustrates adds an optimistic scenario enabled by regulatory clarity and rapid scaling, and a conservative case where near-term skills gaps and governance challenges delay growth before recovery later in the decade.

Mapping Regional Investment and Expansion

Regional momentum is pronounced, with North America and EMEA each accounting for over 40% of global demand and investments. North America’s leadership draws on strong IDP investments in the BFSI, Insurance, and Healthcare sectors, while EMEA’s growth (16%) reflects both Western European digitalization and rapid Middle Eastern investment. Asia-Pacific, with $1.3 billion in spend and 14.5% growth, is propelled by automation initiatives in China and India. Japan remains the region’s largest but more mature, slower-growing market. Latin America posted the fastest increase, at 23%, as both economic improvements and public sector transformation accelerated adoption. These adoption trajectories -shaped by digital maturity, GenAI pilot-to-scale activity, and evolving governance models – will define the next wave of regional advancement.

Vertical Momentum: Leaders, Growth Hotspots, and Sector Dynamics

Finance—including Banking, Financial Services, and Insurance—remains the largest industry, driven by complex use cases in onboarding, claims automation, and compliance. Following two years of above-average growth, demand in 2024 moderated as organizations assessed the opportunities of GenAI technologies and the potential ROI of advanced platforms. The Public Sector ranks second, representing 14% of global investment, buoyed by national and federal digital initiatives, yet local adoption remains uneven due to budget and talent gaps. Healthcare saw accelerated adoption at 12% growth, bolstered by regulatory requirements for real-time access and automation. Manufacturing stood out with the highest growth rate (24.5%), as IDP solves supply chain and compliance pain points. Retail leads second-tier vertical growth due to automation of supply chain and customer-facing workflows, while Logistics, Legal, and Higher Education sector adoption is more measured.

Use Case Evolution: Where Value and Growth Meet Constraints

Case Management remains the largest use-case group at 37% of global end customer investments, driven by demand for efficient onboarding, claims processing, and the need to automate complex, document-heavy workflows. GenAI and Agentic AI is increasingly used to reduce process steps that involve significant manual efforts combined with approval steps in a dynamic business environment. Accounting represents 32% of investment and is in transition: e-invoicing mandates are pushing organizations toward end-to-end P2P/OTC automation, but legacy integration challenges persist. Customer Support has become the fastest-growing use case (20+% YoY), mirroring the shift toward real-time, omnichannel engagement where IDP enables real-time interpretation of emails, chat, and portal inputs at scale. Records Management remains a smaller but strategically important use case, particularly for compliance and analytics. Future opportunities lie in developing knowledge bases that provide context for GenAI-driven automation solutions.

Market Dynamics: Transformation, Automation, and Structural Shifts

The dynamics shaping the IDP market today revolve around three forces: technology innovation, evolving governance, and rising enterprise readiness. GenAI has become a true accelerator, enabling the transition from experimentation to production-grade automation that improves accuracy, reduces configuration time, and supports multimodal content. Retrieval Augmented Generation (RAG) and domain-tuned models underpin cost control and reliability. The next phase, agentic automation, is about embedding AI agents to plan and execute end-to-end workflows under robust enterprise guardrails. The transition from assistive automation to truly autonomous orchestration will increasingly shape competitive advantage, hinging on governance, explainability, and compliance.

At the same time, critical structural shifts are underway. Cloud and subscription models are expected to surpass 50% market share by 2029, lowering deployment barriers and accelerating mid-market expansion thanks to low/no-code configurability and natural language interfaces. Regulatory frameworks like the EU AI Act are making explainability and human oversight central to vendor selection. In Accounting, e-invoicing mandates are shifting opportunities from basic document ingestion to further downstream automation such as validation, reconciliation, and analytics.

Vendor Landscape: Growth Dynamics Along the Maturity Curve

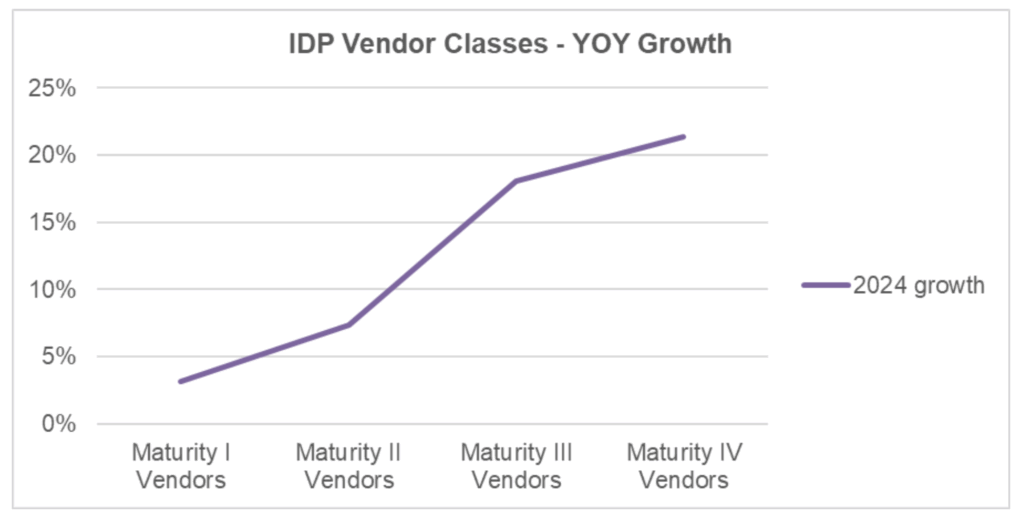

Our assessment of ~ 400 IDP vendors confirms that growth correlates strongly with maturity.

- Level I (Document Capture): Vendors specializing in legacy or niche capture technologies are under increasing pressure. Many face stagnant or negative growth, with some actively repositioning through partnerships or acquisitions to remain relevant.

- Level II (Advanced Capture): These vendors have evolved to include machine learning–based classification and semi-structured extraction but still lack robust governance or meaningful workflow orchestration. While this segment maintains upper single-digit growth, competition is intensifying as buyers demand next-generation solutions.

- Level III (IDP Platforms): Vendors delivering full-stack IDP platforms with built-in governance and GenAI-driven extraction capabilities are seeing wide variability in growth. Established names experience steady, single-digit rates, while AI-native entrants achieve high double-digit expansion by meeting enterprise demands for innovation and flexibility.

- Level IV (Integrated IDP): The fastest-growing cohort, these vendors embed IDP deeply in RPA/BPM or horizontal automation frameworks. Surge in demand for truly end-to-end automation supports annual growth rates above 20%.

- Level V (Autonomous Automation): While no vendor has yet achieved fully autonomous, agentic orchestration at enterprise scale, early pilots—particularly in case management and finance—signal the direction of the market’s next major leap.

This market structure underscores the importance of platform breadth, orchestration, and continuous innovation as enterprise buyers move up the maturity curve. Vendors positioned in the higher maturity tiers are best equipped to capture increasing market demand as end-to-end automation and GenAI-driven strategies become enterprise priorities.

Looking Forward: Strategic Infrastructure, Not Just Software

As the market enters its next chapter, a new divide is emerging—defined by which enterprises and vendors can advance up the maturity curve toward domain-tuned GenAI and agentic orchestration, to realize autonomous end-to-end automation. The strongest growth pockets and new opportunities will arise where sector-specific needs, decision-ready use cases, and input diversity intersect. The IDP space is positioned to deliver measurable ROI and meaningful business outcomes—not just incremental digitalization—as strategic infrastructure for the modern enterprise.

About the Author:

Petra Beck is a Senior Industry Analyst at Infosource, where she leads market analysis and forecasting for Intelligent Document Processing (IDP). She brings over 25 years of experience in Information Management, combining international perspective with deep expertise in research and strategic planning.

To find more news from Infosource, click here.

You may also like:

📨Get IDP industry news, distilled into 5 minutes or less, once a week. Delivered straight to your inbox ↓